Compliance & tax

A handful of US tax and securities rules shape every cap table: a current 409A valuation, the 83(b) deadline, Rule 701 limits, Form 3921 for ISO exercises, and the QSBS clock. Tenacap gathers them on one compliance page so the dates and numbers that matter stay in view — without pretending to be your accountant.

Each company has a Compliance & tax page, linked from the cap-table header, that pulls together the records below. Everything here is informational and built to keep counsel and accountants in the loop, not to replace them — Tenacap produces audit-ready data and reminders, but it never files anything with the IRS on your behalf.

409A valuations

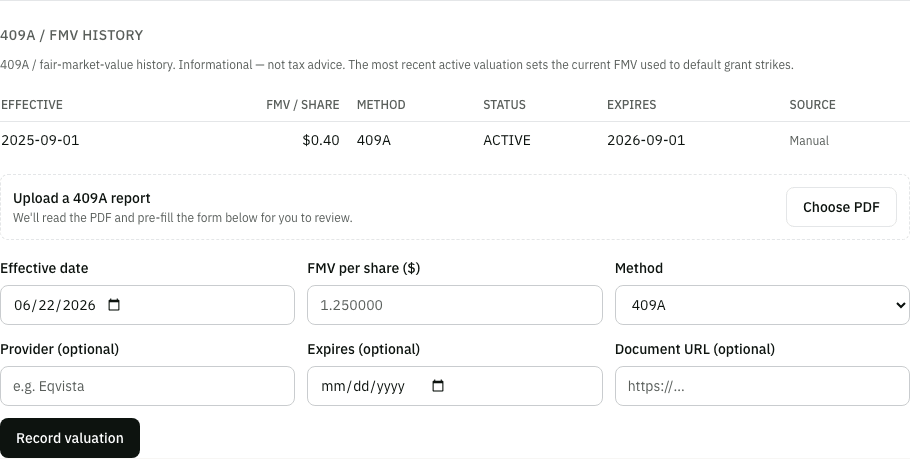

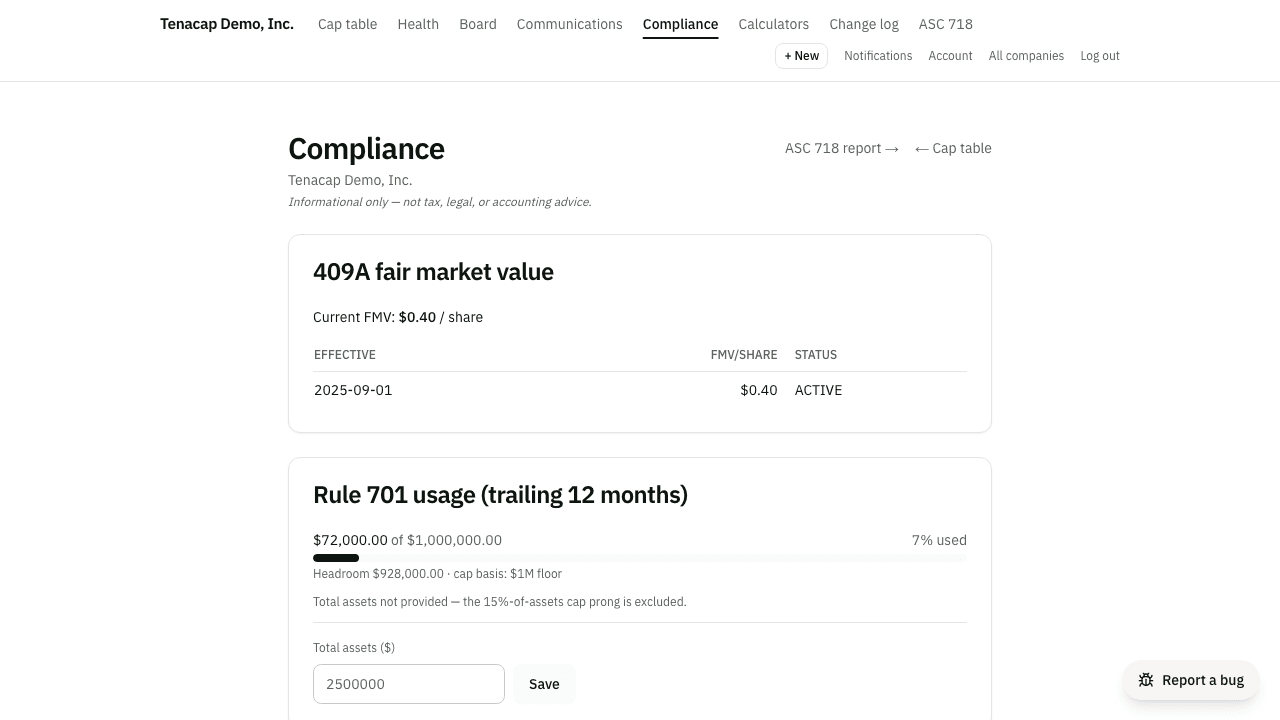

A 409A valuation sets the fair market value (FMV) of your common stock, which in turn drives the strike price of option grants. Record each valuation with its effective date, FMV per share, method (409A, board, or other), provider, and an expiry — most valuations are good for about twelve months or until the next material event. The valuation whose window covers today is your current FMV.

That current FMV does real work elsewhere in Tenacap: it pre-fills the strike on new option grants (and warns you if you set a strike below FMV), it feeds the estimated value shown in the stakeholder portal, and it supplies the FMV-at-exercise used for Form 3921 below.

Import your 409A report

Rather than retype the figures, upload the PDF your 409A provider sent you under Manage → Valuations. Tenacap reads the report and pre-fills the form — FMV per share, valuation date, expiry, provider, and method — so you just review and confirm. Fields we couldn’t read with confidence are highlighted for you to fill in or correct, and we flag the entry if the FMV looks far outside what your cap table implies. Nothing is saved until you confirm, and the original PDF is kept with the valuation as a record.

You don’t have to remember to check the expiry date: Tenacap can email your admins as a 409A approaches expiry (and once it lapses), so you can line up a refresh in time.

83(b) election tracking

An 83(b) election asks the IRS to tax restricted stock at purchase rather than as it vests. When you issue restricted stock, Tenacap creates an election, computes its deadline (the purchase date plus 30 days), and tracks its status: not filed, filed, late, or not applicable. A daily reminder job emails the holder as the deadline nears, and any election left unfiled past its window is swept to late.

Once you mail an election, mark it filed (and optionally attach the letter) so the holding stays accurate. All of a company’s elections, with their deadlines, live in this section.

Rule 701 limits

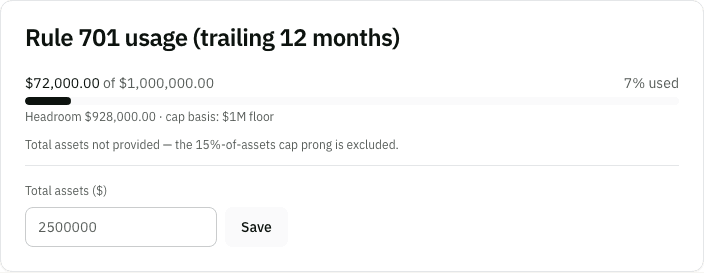

Rule 701 is the federal exemption that lets a private company grant equity under written compensation plans without registering it. It comes with a ceiling on the value you can offer in any rolling twelve months: the greater of $1 million, 15% of total assets, or 15% of the outstanding shares of that class. Tenacap totals the value of grants over the trailing year — using each grant’s FMV at grant — and shows your current usage, your remaining headroom, and a warning as you approach the cap.

Form 3921 export

Companies must file Form 3921 with the IRS for each incentive stock option (ISO) exercised during the year. Tenacap assembles the reportable rows from your exercise records — grant date, exercise date, strike price, FMV at exercise, and share count — and gives you a year-end CSV export per employee plus a company summary. Where an exercise crosses the $100,000 ISO limit, only the ISO-qualified portion is reported; the rest is treated as a nonqualified option.

The export is meant to hand to whoever files for you. Tenacap produces the data; the filing itself stays with the company or its provider. Related ISO figures on this page — the $100k limit split and the AMT preference on exercise — are informational estimates to help you and your advisor see what an exercise might trigger.

The QSBS clock

Qualified Small Business Stock (QSBS) can let shareholders exclude a large share of their gain from federal tax — but only if the stock is held for more than five years, among other conditions. Tenacap surfaces a per-holding QSBS summary with a five-year clock and eligibility flags, so you can see how close each holding is to the threshold. It’s a heads-up, not a determination: QSBS eligibility turns on facts Tenacap can’t fully verify.