Exit waterfall

When you sell the company, the proceeds don’t split by ownership percentage — preferred investors get paid first, on the terms they negotiated. The exit waterfall takes an acquisition value and works out who actually walks away with what, so you can answer that question before you ever sign a term sheet.

Ownership percentage tells you how the company is divided. It does not tell you how the money is divided when the company is sold. Preferred shareholders almost always have a liquidation preference — a right to be paid back first, often a multiple of what they put in — before common shareholders see a cent. The exit waterfall runs that whole payout, in order, for an exit value you choose. Like scenario modeling, it’s a private projection: it reads your live cap table and never writes a record.

Open the waterfall

From your cap table, open Exit waterfall — it sits in the cap-table header right next to Model a round. The screen is read-only and available to anyone with view access, so you can share it in a board meeting or hand it to an investor without worrying that someone will change your records.

Enter an exit value

There’s a single input: the exit value — the total proceeds from the acquisition or liquidation, in dollars. Type a number (commas and a dollar sign are fine, for example 50,000,000) and press Run waterfall. The calculation runs over a snapshot of your company exactly as it stands today, so change the number and run it again as often as you like.

How preferences stack

Preferences are paid senior first. Each preferred share class has a seniority rank; the most senior class is paid its full preference before the next tier sees anything, and so on down to common, which is last in line. Within a single tier, if the proceeds run short, the available money is split pro rata across the classes in that tier.

A class’s preference is its liquidation-preference multiple times the amount actually invested in it — the per-share price multiplied by the shares outstanding, summed across every lot. A 1× preference returns the investment; a 2× preference returns twice it. You set these rights — seniority, multiple, participation — on the preferred class itself when you record a priced round. Voting-only or non-economic classes are left out of both the preference stack and the residual entirely.

Convert or take

Non-participating preferred face a choice the waterfall makes for them automatically: take the liquidation preference, or give it up and convert to common to share in the residual — whichever pays more. At a low exit value the preference wins. At a high enough value, the as-converted common stake is worth more than the preference, so the class converts. The model resolves every class’s decision together (one class converting changes the maths for the others) and shows a converted to common note next to any class that chose to convert.

Participating preferred & caps

Participating preferred get the best of both worlds: they take their preference and then also share in the residual pro rata with common, as if they hadn’t been paid the preference at all (“double dip”). To keep that in check, a participating class can carry a participation cap — a ceiling on its total return, expressed as a multiple of what it invested. When the cap would bite and simply converting to common pays more, the class converts instead. The results split each class’s payout into a preference column and a participation column so you can see exactly where the money came from.

Options, warrants & dividends

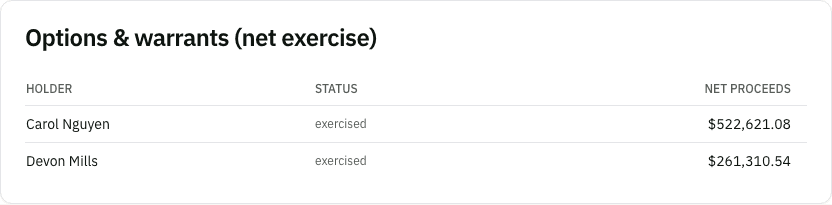

Outstanding options and warrants participate by net exercise. An in-the-money grant exercises: it adds its shares to the residual pool and its aggregate strike price into the pot, and the holder nets out the strike — they receive (per-share proceeds − strike) × shares. Out-of-the-money grants simply sit out. When any grants are in the money, a separate Options & warrants table shows each holder, whether their grant exercised, and their net proceeds.

If a preferred class carries cumulative dividends, the accrued amount rides along with the preference. The waterfall accrues simple interest on each lot from its issue date to the exit at the class’s dividend rate, and pays it out senior alongside the preference. Like the preference itself, those accrued dividends are forgone if the class converts to common.

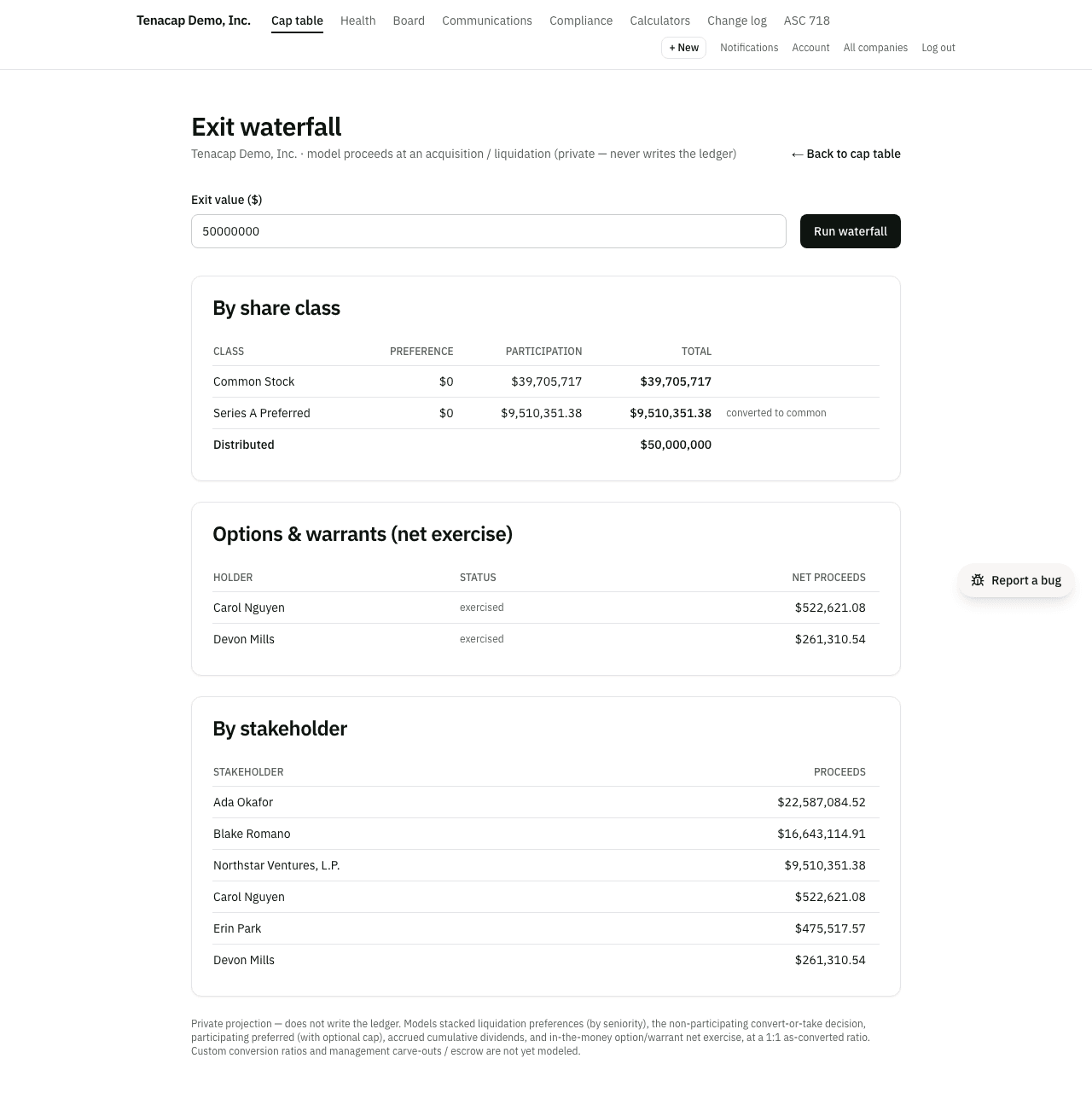

Reading the results

You get three views of the same payout:

- By share class — each class’s preference, participation, and total, with a converted-to-common flag, footed by the total distributed.

- Options & warrants — the net-exercise breakdown, shown only when at least one grant is in the money.

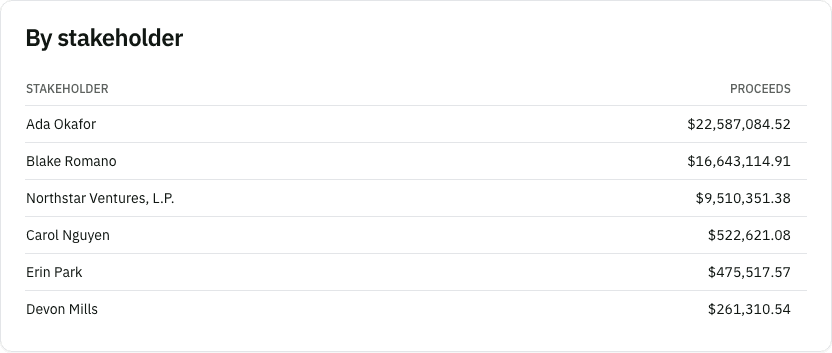

- By stakeholder — each class total split across its holders by share count, plus each exercised grant’s net proceeds, sorted largest first. This is the bottom-line “who gets a cheque for how much” view.

For a forward-looking view of a financing rather than a sale, see scenario modeling. And whenever you need the underlying figures in an open format, you can take everything out from Export & open schema.